Disclosure is key to the house selling process. While the form may seem overly long and confusing, filling it outright is important. Failure to disclose some problems or entering false information can leave you open to a lawsuit, even after closing.

Federal, state and local

You must obey federal, state and local laws for disclosures. There aren’t many federal requirements, but one very significant one is lead paint disclosure. If your home was built before 1978, you must disclose any known lead paint in the house and provide potential buyers with an EPA pamphlet.

As for state and local laws, these vary across the country. Common disclosure requirements include:

Pest infestations

Water infiltration

Mold

Smoke damage

Structural problems

Environmental hazards

Death in the home

Put it in writing

Disclosures must be in writing for potential buyers. Verbal disclosures, no matter how thorough, don’t count.

Patent vs. Latent

When filling out a disclosure form, you may see the terms patent and latent. A patent defect is visible and usually doesn’t need to be disclosed, while a latent defect is hidden and should be disclosed.

What if it’s been fixed?

In most cases, even if you’ve completely remediated the problem, you still need to disclose it as part of the house’s history.

REALTORS® to the rescue

With a qualified local REALTOR®, you’re much less likely to make a mistake during the disclosure process. They can help you identify what needs to be disclosed, when it’s appropriate to say that you simply don’t know, and more.

Recent events have made the spaces in our homes more important than ever—to our productivity, well-being, health and comfort. As we head into a new future, how can we make sure that our homes serve us better?

While homes have always been central in our lives, they have never had to shoulder as much of a load as they have this past year. Since the stay-at-home orders, our homes have had to provide us with everything we need, much of which they were not designed for—from office spaces to classrooms, gyms and sanctuaries.

Our relationships to our home environments have changed, and the psychological impact of being at home, becoming familiar with the new demands on our spaces, and being confronted with all of our “stuff” is not a minor thing.

The effects of this reassessment of our home spaces on our behaviors have been numerous: from making small changes, like seeking to repurpose the spaces in our homes for more practical use (work, recreation, quiet time), or removing various unneeded furniture or objects from our homes, to larger decisions like moving to a house that is more suitable for our own personal indoor-centric lifestyles.

Now, the number of vaccinated Americans is increasing, and a pinprick of light is growing stronger at the end of the COVID tunnel. Does this mean that we will return to pre-pandemic behaviors and forget the adjustments that we’ve made in our homes?

Sally Augustin, an environmental and design psychologist, uses the practice of science to inform design projects in both commercial and residential spaces. She believes that, while we will be glad to be out of our homes again when things become slightly more relaxed, we will also use what we’ve learned from the recent past to inform how our spaces should work for us moving forward.

“We’re a social species, so we like to mix with others,” Augustin says. “We’ll go back to work; we’ll start to see our families again. We’re all pretty sick of our own cooking and all the things we can get delivered, so we’ll go out to eat again. I think people will resume, to a large extent, their previous lives, but they won’t forget their current experiences.”

So, what does that mean for how we design and live within our existing homes, and what we should look for in future property purchases?

SMALL CHANGES

For those who are working within the confines of the spaces that they already have, there are small changes that can be made that will make a significant impact on quality of life at home.

Augustin is quick to list a few things that can make a big difference—noting that they’re not new design elements born out of the pandemic, but rather things that have always helped us to create healthy and happy living spaces, and that can be implemented to great effect in these changing times.

“For most of us, happily, all of our sensory systems are working at same time,” Augustin says. “Always think about the full range of sensory experiences you’ll have in a space.”

To create a more relaxed environment, Augustin recommends playing nature soundtracks at a very low volume in your office or living room. And she says that smell—yes, smell—can also play an important part in how comfortable you feel at home.

“There’s been a lot of rigorous research done on smell and how it affects what goes on in people’s heads,” she says. “You might consider making your home office smell like lemon, which has been linked to cognitive performance. Throughout the home, you might want a lavender scent, because the research shows that the smell of lavender is relaxing.”

Most of us default to sight as the primary sense when we evaluate a space for suitability, and there is plenty you can do to improve the visual impact of your home environment.

“Seeing wood grain is great at alleviating our stress—whether it’s on floors or other surfaces in our homes,” Augustin says. “Relatively light and unsaturated colors (which have always been good for use in a home) are still good. And natural light is like magic for us as humans. Being in natural light improves our cognitive performance—even our creative thinking. Plants were great inside before, and they’re great inside now, in terms of helping us refresh mentally and feel calmer.”

On top of color and light, Augustin notes that the way that we allow our belongings to dominate a space can have a big effect on our mindset.

“It’s really important to think about visual clutter in a space,” she says. “I think sometimes people let that get on top of them. I’m not talking about creating a place that’s stark—being in white box without much going on visually stresses us out—but you’re really looking for a middle ground.

“You want to think through the palette of colors that are in a space, make sure it’s well-managed, have only a couple of patterns in a space, have some personalizing objects on tabletops or hanging on walls, like photographs or art, but don’t let things get away from you.”

Rebecca West, interior designer and founder of Seriously Happy Homes, agrees, adding that clutter can take your space away from you.

“People used to have all these spare rooms, like the guest room or the home gym that wasn’t used much,” she says. “Now, that space has become so much more precious. The demands on the space have become a lot more profound, and people are thinking, ‘This is our reality now. How do we make it work?’

“If you’ve got a space that has been storing stuff that you haven’t touched in five or 10 years, you really got to think, ‘Could I use that space better?’” she says. “This is very helpful for people who feel like they don’t have enough house. You’re just seeing it with blinders on, having lived there for so long that you can’t necessarily see any other way of using the space.”

West notes that, until recently, it’s been much easier to ignore the things in our homes that weren’t working.

“I think that a lot of people were able to ignore that psychological baggage in their home, because they always left the house for work, or they could go out with friends,” she says. “[Since the pandemic], they haven’t been able to escape those psychological cues anymore.”

To create a space that best serves your well-being, West recommends taking a look around your home,

and identifying the things that don’t make you feel good.

“You can take action on the stuff that has been nagging at you, but you weren’t really able to put your finger on,” she says. “Figure out what makes you happy and showcase it, because half the time we hide the stuff we love in a box in the garage. Get rid of the stuff that seems like it should be functional—maybe it was expensive, maybe you have guilt because it was given to you as a gift—but doesn’t make you happy. Who are you serving by holding on to all that?”

Once you have assessed the elements you can bring into your home for well-being, as well as those you should get rid of, the job is not done—you still need to keep on top of what’s coming into the house, and make sure you keep shifting things out, West says.

“A house is never done, because the people in it are always changing, and there’s always stuff flowing in—whether that’s junk mail or groceries or Amazon purchases,” she says. “If we don’t think about the house as this living, breathing organism—where things are breathed in, so they must be breathed out—then we either end up with a totally stale house, or we end up with too much stuff.”

THE BIGGER PICTURE

While there are several things that you can do to improve your space that don’t require remodeling or moving house, sometimes taking a big step and making those larger changes is necessary.

Both West and Augustin note the need, during times when we’re spending more time indoors in close proximity to others, for spaces that can be closed off for work or quiet, but that won’t make residents feel closed-in.

“There’s this competing priority of, ‘I need a door to close so that I can take whatever meeting, or find a mental quiet space,’” West says, “but also, ‘I don’t want to feel super isolated, or trapped in a lot of tiny, small spaces.’”

She says that we can have both space and sanctuary, through having large rooms that can be segmented if necessary—using things like barn doors, sliding doors and room dividers.

“A lot of people will have memories of this event that will guide their future actions. The next time they’re looking to buy a house, they’ll make sure it has some space where they can work effectively from home. People will perhaps be looking for spaces with a little more internal segmentation from one space to another, because they’ll remember how nice it was to be able to isolate a bit when they were confined to their home with all the members of their family for weeks on end.”

Aside from the practicalities of working and schooling from home, we should also look for spaces that prioritize our mental and physical health, West says.

“I certainly think that people will be looking beyond the footprint of their home. Walkable neighborhoods and outdoor spaces are more important than they were pre-pandemic. It’s about the home, but it’s also about what’s outside your home. Do you have an outside gazebo or some outdoor space where you could have friends over if you’re worried about social distancing?”

West also recommends thinking about the multigenerational living that many of us are now doing, and making sure that there are spaces that are useful to the different members of the household—things like study spaces for children, workout rooms for active people, hangout areas for the family, and comfortable quarters for elderly relatives.

“Then there’s privacy,” she says. “What do the windows look out onto? Are they looking into your neighbor’s home? Will that make you feel more trapped? And what kind of light are you going to be getting throughout the day, especially during the hours you want to be more alert or more rested?

“As you’re looking at a new house and trying to imagine your furniture in the space, really go through the exercise of thinking, ‘Where would I sit in this room? How would it feel for me to sit in this room while spending 12 hours working in this space?’”

For Augustin, the senses are again an important consideration when evaluating a home for suitability.

“When you first see a home that you might buy, often you’re looking at like an online listing, which is pictures. But make sure you read the words, too, because maybe you’ll find out that the house is next door to a preschool or something. Some people might love the sound of little kids laughing in the morning, but if you’re going to be up all night because you’re an emergency-room physician, maybe you don’t want to live next door to a preschool.

“There was a neighborhood in Chicago that for decades smelled like chocolate because it was right near the Brach’s Candy Factory. It was a perfectly nice neighborhood, but if you didn’t like chocolate or [had dietary health concerns], that probably wasn’t the place for you.

“In general, keep in mind that your house is more than what it looks like.”

Beyond what a house can offer in terms of practical considerations, there’s the need for us to feel… well, at home. In a time when security and safety are top of mind for most people, familiarity can provide comfort. So how can you create that feeling in a brand-new home, which is—at least to begin with—unfamiliar?

Augustin recommends giving thought to what makes your house really feel like home to you. “If you can continue to use the same furniture, or look at the same art, that increases feelings of familiarity and safety,” she says. “Is your furniture or your art going to fit in the new home? If you’re coming from an apartment with lots of solid, interior walls, and you go to a home that’s open plan, with very few interior walls and lots of windows, you’re not going to be able to hang as many paintings. If that art is meaningful to you, a new home where you can’t put it up and see it is not going to be the best place for you to be.

“You have to think through where you were already, your good experiences there, and how many of those you’ll be able to carry through to the new space to make it familiar. If you’re going to make a big change, why? Is it likely that you will be happy after you make it, based on where you’ve been happy previously?”

Home is the most personal space that any of us have, and we need to make decisions according to what feeds our own individual sense of well-being. Identify the things that make you feel comfortable, make your home feel practical, and ensure that it serves you and your family in the best way possible. Then, make the necessary changes, or, if you need to, purchase a house with those things in mind. In a nutshell, create your space intentionally.

Or, as Augustin says, “Just manage things. Be active. Take control. Don’t let your house just happen to you.”

Trending: 10 home features that have fallen out of favor:

1. Bold color schemes

2. Industrial-style kitchens

3. Kitchen islands

4. Granite countertops

5. TVs in the kitchen

6. Over-the-stove microwaves

7. Raised-panel cabinets

8. Wall-to-wall carpet

9. Distressed wood walls

10. Mediterranean-inspired suburban McMansions

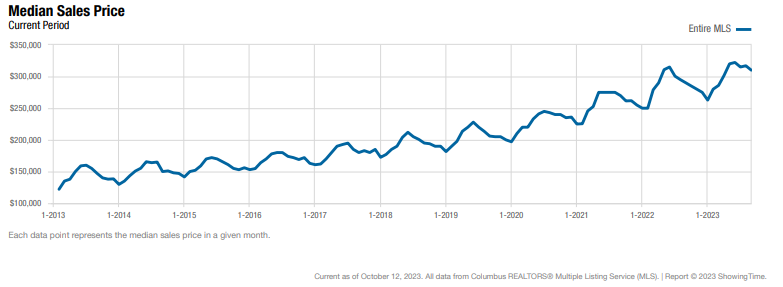

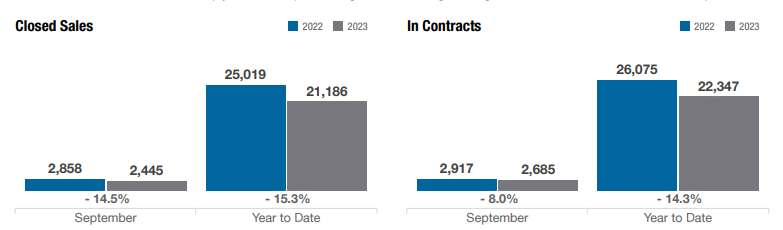

SEPTEMBER SAW A 14.5% DECREASE YEAR OVER YEAR IN CLOSED SALES, BUT INVENTORY ROSE 5.5% OVER AUGUST.

COLUMBUS, Ohio (Oct. 19, 2023)— There were 2,445 sales and nearly 2,900 new listings added to the market, according to the latest central Ohio housing report provided by Columbus REALTORS® for the month of September 2023.

Year – Over – Year Comparison

In September 2022, there were 2,858 closed sales with a median sales price of $290,000. One year later, the region witnessed a 14.5 percent decline in sales while experiencing a 6.9% increase in median sales price, up to $310,000.

There were 2,875 new listings added to the Columbus and Central Ohio Regional MLS in September, and the total inventory of homes for sale in the MLS sits at 3,624, slightly lower than the 3,806 homes available one year ago.

“Last year, when the market was at an all-time high, we expected some leveling off,” said Columbus REALTORS® President Patti Brown-Wright. “I think that the market has adjusted in a way that’s been gradual, and we’ve all had to adapt.”

Mortgage Rate Impact

One of the most significant factors in the market has been the rise in mortgage rates over the last 24 months. In two years, consumers have gone from record-low rates of under 3% to mortgage rates not seen since the millennium. This may be the perfect time for everyone involved in real estate to have some perspective.

“I think many of us remember the 1980s when mortgage rates were 16%, but we have to remember that most prospective buyers in today’s market do not remember those days. Over the last two decades, mortgage rates have been mostly under 5%. This is the world the majority of the public has come to know.”

According to data from Freddie Mac, the average 30-year fixed mortgage rate in 1975 was 9.05%. Rates peaked in 1981 at 16.63% and remained in double digits until 1991, when they dropped to 9.25%. The first time the average 30-year fixed mortgage dipped below six percent was in 2003 at 5.83%. That ushered in a 20-year era with an all-time low of 2.96 percent in 2021.

Local Spotlight

Hilliard has 105 active homes on market. With an average days on market of 16 days, the market has the shortest sales cycle of west side suburbs. The average price for Hilliard homes through $401,750.

Dublin has 153 active homes on the market. With the highest average sales price of $519,203 on the west side, days on market holds at 21.

Grove City has 174 active homes on the market. Grove City holds the dubious title of highest of number days on market at 29 in spite of having a low average sales price of $351,367.

“REALTORS® have to know their history,” continued Brown-Wright. “The average 30-year mortgage rate since Freddie started tracking this in 1971 is just under 7.74%. Today’s current rate is *7.80%. That may not be a nice warm blanket for today’s buyer, but it’s the facts. Where REALTORS® can make an additional impact is connecting their customers with lenders offering products that can provide relief at the negotiating table. Understanding your financing options should be the top priority for today’s buyer.”

Columbus REALTORS® is composed of almost 10,000 real estate professionals engaged in residential and commercial sales and leasing, property management, appraisal, consultation, real estate syndication, land development, and more.

The Columbus REALTORS® Multiple Listing Service (MLS) serves all of Franklin, Delaware, Fayette, Licking, Madison, Marion, Morrow, Pickaway, and Union Counties and parts of Athens, Champaign, Clark, Clinton, Fairfield, Hocking, Knox, Logan, Muskingum, Perry, and Ross counties.

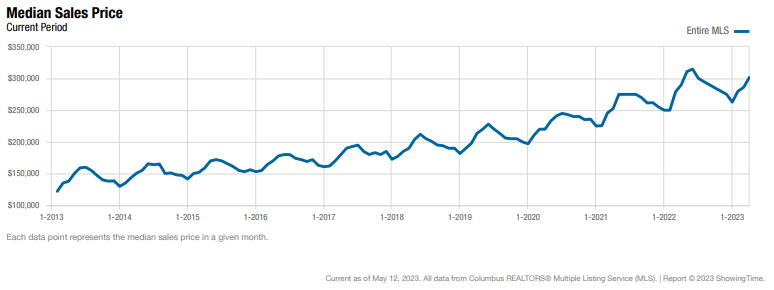

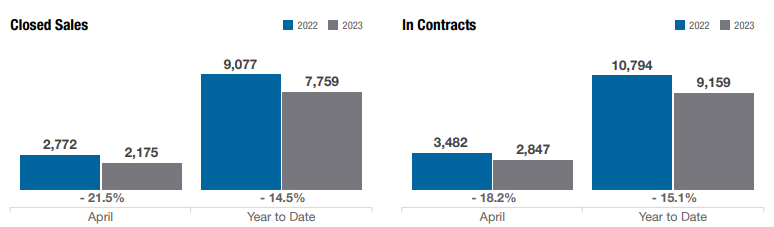

For April 2023, the median sales price in central Ohio rose above $300,000 for the first time since July of 2022 in the latest housing statistics for April 2023 from Columbus REALTORS®.

The median sales price rose 4% year-over-year and 5.5 percent month-over-month. This is only the fourth time that the median sales price has crept over the $300,000 mark since statistics began being tracked by Columbus REALTORS®. The other three occurrences were in May of 2022 ($310,830), June of 2022 ($315,000), and July of 2022 ($300,563).

Year-Over-Year Decrease

There were 2,175 closed sales in April, a 21.5% decrease year-over-year and a 5.6% decrease compared to March.

“May of 2022 was right about the peak of the market in central Ohio. At that time last year, we had even less inventory than we do right now, and homes were selling in 13 days,” recalled Columbus REALTORS® President Patti Brown-Wright. “We know that mortgage rates are higher, but the housing market in central Ohio is still very much in-demand.”

Strong Demand / Low Inventory

In April, the average number of days on the market dropped to 24. In March, homes averaged 34 days on the market. The percentage of the last list price received also ticked up to 101.1%. Last year, at the market’s peak, homes sold for nearly 5% over asking.

“Inventory is playing a big part in all of this,” noted Brown-Wright. “A balanced housing market requires about 5-6 months of inventory. We have less than a month of inventory, so central Ohio remains a strong seller’s market.”

Inventory Driving Prices Up

In April, the average number of days on the market dropped to 24. In March, homes averaged 34 days on the market. The percentage of the last list price received also ticked up to 101.1%. Last year, at the market’s peak, homes sold for nearly 5% over asking.

“Inventory is playing a big part in all of this,” noted Brown-Wright. “A balanced housing market requires about 5-6 months of inventory. We have less than a month of inventory, so central Ohio remains a strong seller’s market.”

Interest Rates Play a Part

Rates on a 30-year fixed mortgage hovered slightly over 7% in April, and according to statistics from the Central Ohio Regional MLS, 20% of all closed sales in April were cash sales, while 65% were conventional mortgages and 16% were government-backed loans.

Local Spotlight

In the local market spotlight, homes in the Dublin Local School District (LSD) covering Franklin, Deleware and Union Counties saw just 73 closings in April versus 119 in 2022, a 38.7% drop year-over-year. For the year, the market is down 23.5% with just 250 homes sold versus 350 in 2022. Predictably, the average price, $523,659, and median , $435,000, prices were both up in April compared to last year. Along with the price and interest increases, days on market expanded from 8 days to 19 days.

Homes in the Hilliard CSD School District (CSD) covering Hilliard and parts of Prairie Township saw just 97 closings in April versus 109 in 2022, an 11% drop year-over-year. For the year, the market area is down 10.8% with just 298 homes sold versus 334 in 2022. Predictably, the average price, $378,706, and median , $385,000, prices were both up in April compared to last year. Along with the price and interest increases, days on market expanded from 5 days to 13 days.

Homes in the South-Western City School District (CSD) covering Franklin and Pickaway Counties and including Grove City and Galloway saw just 116 closings in April versus 187 in 2022, a 38% drop year-over-year. For the year, the market area is down 17.4% with just 476 homes sold versus 576 in 2022. In a reverse to many of the areas markets,, the average price, $303.159 fell 2% compared to April of 2022. Median price rose to, $287,950, prices rose 4.7% in April compared to last year. Along with the price and interest increases, days on market doiubleed from 14 days to 28 days.

Marion saw a 19% increase in closed sales (50). The average sales price in Marion was $165,667, roughly half the cost of the average sale price in central Ohio. Big Walnut LSD in Sunbury also saw a 50% rise in closings as their average sales price climbed 16.2% to $533,230 in April. Of the 2,175 closings in central Ohio, 54% occurred in Franklin County, where the average sale price increased 2.5% to $340,434.

About Columbus MLS

Columbus REALTORS® is composed of almost 10,000 real estate professionals engaged in residential and commercial sales and leasing, property management, appraisal, consultation, real estate syndication, land development, and more.

The Columbus REALTORS® Multiple Listing Service (MLS) serves all of Franklin, Delaware, Fayette, Licking, Madison, Marion, Morrow, Pickaway, and Union Counties and parts of Athens, Champaign, Clark, Clinton, Fairfield, Hocking, Knox, Logan, Muskingum, Perry, and Ross counties.

Here for You

If you are considering selling your home or looking for your next, I can help! To request a free complete guide to selling your home or a competitive market analysis click here. To find available homes by school district, click here.

THE REGION SAW A 33 PERCENT BOOST IN CLOSED SALES MONTH-TO-MONTH.

March signifies the start of Spring, and the central Ohio housing market saw a significant uptick month over month. There were 2,304 closings in March as the average sale price increased to $328,769. In February, there were 1,728 closed sales marking a 33 percent increase month to month.

Columbus Ranks 4th Nationally

Columbus moved up one spot on the Realtor.com Top 20 Hottest Housing Market list, jumping from fifth place in February to fourth in March. The Hottest Housing Markets are based on market demand, as measured by unique views per property on Realtor.com, and the pace of the market, as measured by the number of days a listing remains active on Realtor.com.

In March of 2022, there were 2,430 closed sales, which equates to a 5.2 percent decrease yearly. The average sale price one year ago sat at $318,826. With the average increasing by over $10,000, the average sale price is up 3.1 percent over last year.

“Home prices continue to tick up each month around Columbus,” said Columbus REALTORS® President Patti Brown-Wright. “That can pose some challenges to potential buyers, but it’s also important to remember that Columbus remains one of the most affordable metros in the U.S.”

According to the Bankrate.com Cost of Living Comparison Calculator, living in Columbus is 40 percent lower than in Seattle, 19 percent lower than in Denver, 41 percent lower than in Washington, D.C., and 3 percent lower than nearby Indianapolis.

For the better part of two years (2020-22), central Ohio homebuyers became accustomed to homes selling for slightly over the asking price. Last year the percentage of the last list price received sat at 103.5%, and this month the average is back over asking at 100.3%.

Home sales are rising, and days on the market are dropping. 72.6 percent of homes sold in 30 days or less in March. On average, homes last 34 days on the market, but that isn’t the case in some of central Ohio’s hottest suburbs.

There were 82 closed sales in Westerville City School District in March, and homes were on the market an average of 16 days. Dublin (Corp.) saw 33 closings, and homes were sold in 10 days last month.

Even with Escalating Prices, Columbus is Still Affordable

In the Hilliard School District, there were 74 closings, down from from 96 last March, and homes were on the market for 23 days compared to just 8 days for the same period last year. Home prices, however, continue to rise, up .5% to $359667.

“The competition is still fierce out there,” said Brown-Wright. “With mortgage rates still hovering around 7 percent, there are not as many new listings coming onto the market as there were at this time last year. Buyers need to act fast.”

There were 2,630 new listings in March, a 20 percent drop over 2022 when rates were 3-4 percent lower. The decreasing number of new listings has the total inventory at 2,322 homes in central Ohio.

For the second-straight month, South-Western Consolidated School District in Grove City has remained hot with 151 closed sales at an average sales price of $310,138, up 13.4 percent year over year. Olentangy Local School District in Delaware County has kept up its torrid pace with 111 closings with an average sale price of $584,123, a 10.1 percent increase over March 2022.

“We’re heading into peak season for buying and selling in central Ohio,” noted Brown-Wright. “REALTORS® are there to help potential buyers and sellers navigate this challenging market, so don’t hesitate to reach out.”

Like last month, Ohio boasts five metros in the Realtor.com Top 20. Columbus (4th) leads the way, followed by Dayton (11th), Akron (15th), Canton-Massillon (16th), and Toledo (17th).

If you are considering selling your home or looking for your next, I can help! To request a free complete guide to selling your home or a competitive market analysis click here.To find available homes by school district, click here.

Coming into Spring, it’s time to see where the market stands.

The average sales price in Dublin. is $481,276. Days on market is 25 days. Homes in Dublin are selling at .6% over list price.

The average sales price in Hillard stands at $372,237. Homes here are selling at the fastest clip on the west side at 18

days on market and at the highest rate of the .7% over list price.

Galloway average sales price average at $290,658. Days on market is 24 days Homes in Galloway are selling at an impressive 2.1% over list price compared to its pricier neighbors.

The average sales price for homes sold in Grove City is $350,246. Days on market rose is longest on for the west suburbs at 34 days, with homes selling at .4% over list price.

The smallest suburb (and likely the most resistant to being called a suburb), West Jefferson, average sold price settled at $278,775. Days on market ties for shortest with Hilliard at 18 days. West Jeff also holds the dubious distinction of being the only suburb where sold prices fall below list prices at -.02%.

If you are considering selling your home or looking for your next, I can help! To request a free complete guide to selling your home or a competitive market analysis click here.

On May 1, 2023 changes to the Level Price Adjustments (LLPA) will impact the interest rate you pay on mortgages. Because the mortgages written over the next few months will be eligible for purchase by Fannie Mae and Freddie Mac in the pursuing 60 days, lending institutions will begin using these guidelines as early as April, or sooner depending on the lender. It’s kind of wonky, but it really helps to understand how the lender arrives at the number you pay. The lending institution lends you money. They also want it insured so that if you default, they do not lose the principal.

Fannie and Freddie

Fannie Mae was charted by the U.S. Congress in 1938 because leaders wanted promote home ownership by making it more affordable. The principal mechanism was to make long-term mortgage loans more attractive to lenders by allowing smaller down payments.

Freddie Mac was charted by the U.S. Congress in 1970 after Fannie Mae became a private shareholder-owned corporation. The purpose was to divide the monopoly position Fannie Mae posed.

While the percentage changes year to year, since 2002, Fannie Mae and Freddie Mac bought and bundled anywhere from 55-64% of mortgages. They purchase mortgages from lenders, package them into securities, and sell those securities to investors. This keeps money flowing back into lending institutions so the have ample funding to extend more loans and help more people by homes (source).

Variables

There are many variables that drive the interest rate you pay. Below are some of the larger variables:

Economic indicators: Changes in the economy, such as inflation and unemployment rates, can impact mortgage interest rates.

Federal Reserve policy: The Federal Reserve can raise or lower interest rates to control inflation, which can in turn affect mortgage interest rates.

Lender’s risk tolerance: The riskier the loan, the higher the interest rate will be to compensate the lender for taking on more risk.

Loan type: Different types of loans, such as fixed-rate or adjustable-rate mortgages, can have different interest rates.

Loan term: The length of the loan, typically 15 or 30 years, can impact the interest rate.

Down payment: A larger down payment can reduce the amount borrowed, making the loan less risky for the lender and potentially resulting in a lower interest rate.

Credit score: A higher credit score can indicate to the lender that the borrower is a lower risk, potentially leading to a lower interest rate.

Property type: The type of property being purchased, such as a single-family home or a multi-unit building, can impact the interest rate

Next week, I will dive into how the LLPA weigh these factors and how they impact how your lender may recommend you structure your mortgage.

These are some of the key variables that can impact mortgage interest rates. It’s important for homebuyers to understand these factors and to work with a lender to determine the best mortgage options for their specific needs and financial situation.

If you are considering selling your home or looking for your next, I can help! Click here for a quick guide to home staging success. To request a free complete guide to selling your home or a competitive market analysis click here. If you are considering selling your home or looking for your next, I can help!

To explore available homes in the Columbus metro, click here.

Housing affordability and availability are major concerns across the United States. Here in my hometown of Columbus, Ohio, it is the same. We enjoy a growing population and economy thanks to projects like Intel’s $20 billion dollar investment in a new production facility.

According to a 2022 Building Industry Association of Central Ohio study conducted by Vogt Strategic Insights, we need 14,000 – 19,000 new homes each year. Which is roughly double the current number of new homes built in the region. In a recent interview (1/27/2023), Lawrence Yun, Chief Economist for the National Association of Realtors, builders face two major obstacles. Limited lot availability and a worker shortage. Because of these, and other factors, new homes are more expensive than existing homes.

This means that new homes are generally out of reach for first-time buyers. So, to make room for first-time buyers, an existing home must become available. Existing homeowners are reluctant to sell their existing home for a couple of good reasons. First, they are concerned about interest rates. Why sell their existing home, even if it does not meet there needs or desires if they have to pay a higher interest rate. Second, if they sell, where will they move to? In a recent survey of builder’s websites, I located over 100 new communities in the Columbus metro. The homes start at in the mid-$300’s and topped out as far as your budget can handle. The square-footage of the homes start as low as 1419 and expanded to nearly 6000. There are some advantages to buying new construction. According to Gonzalo Mejia, a Realtor in Jacksonville, Florida, they are:

The ability to customize, select the floor plan and finishes.

You get to pick your lot.

Everything is new. You have peace-of-mind of not having to deal with things breaking down or needing replaced.

The price is only one factor – the sales price may be higher, but energy efficiency means lower energy bills, lower maintenance costs and a long time before you must replace anything.

Newer technology – higher internet speeds

Builders work with lenders or have in-house financing. This may mean a lower interest rate.

The builder may pay down points.Lock-in interest rates to accommodate longer build time.

Available inventory. Even in this tight market, builders have inventory homes that are ready to move into as soon as 60 days.

The choices can be overwhelming. This is why should you work with a Realtor when looking at new construction. A Realtor that specializes in new construction is familiar with the communities and promotions each builder offers and can help you find a community in the area you want to live in, with the features you want and at a price that meets your budget.

If you are considering selling your home or looking for your next, I can help! Click here for a quick guide to home staging success. To request a free complete guide to selling your home or a competitive market analysis click here. If you are considering selling your home or looking for your next, I can help!

To explore available homes in the Columbus metro, click here.

Source: Columbus Realtors

Homebuyers have more options in central Ohio, and mortgage rates take a welcomed dip. Columbus REALTORS® breaks down the December housing report for central Ohio.

The average sales price has increased by 9.4 percent since last December, up to $318,581. On average, homes sold for just over $27,000 more than last year in central Ohio. The median sales price also saw a 7.8 percent spike, rising from $255,000 in 2021 to $275,000 in December 2022.

“Home sellers are seeing big gains in their bottom line if they have patience with their home sale,” said Sue Van Woerkom, 2022 President of Columbus REALTORS®, “This market is not as fast and furious as what we saw early this year. Homes are sitting just a little bit longer.”

Homes spend an average of 29 days on the market. That is up from an average of 18 days last year at this time. Even with just over one month of inventory in central Ohio, the region remains a strong seller’s market.

“Despite this being a seller’s market, buyers do have their pick right now. Homes are sitting on the market a little longer, giving people more time to make sure they are investing in the right property,” said Van Woerkom.

As Van Woerkom references, buyers have more options to choose from this winter. Inventory rose 36% compared to December 2021. Several communities saw an influx of new homes for sale. The list includes the Columbus suburbs of Clintonville, Grandview Heights, and New Albany.

Sellers in rural counties are benefitting from a surge in their property value. Properties in Fayette County saw their average home sale price jump by nearly 50 percent in December. Champaign, Ross, Hocking, and Ross County sellers also benefited from rising home prices.

One segment of the population that has faced challenges in the changing market has been first-time home buyers. December began with the 30-year fixed-rate mortgage averaging 6.49%. The rate dip has helped, but the prevailing feelings of economic uncertainty exist. Still, National Association of REALTORS Deputy Chief Economist and VP of Research Dr. Jessica Lautz sees opportunities on the horizon for first-time home buyers in 2023.

“There was a frenzied pace in the housing market, which had pushed first-time buyers, often with FHA or VA mortgages, to the sidelines. As some buyers have retreated, high-income, first-time buyers may take advantage of the market right now,” said Lautz.

In reference to current interest rates, Van Woerkom has this advice for potential buyers.

“We aren’t near the rock bottom rates we’ve seen, but working with an experienced REALTOR® can guarantee you will get the best rate based on your needs,” said Van Woerkom.

If you are considering selling your home or looking for your next, I can help! Click here for a quick guide to home staging success. To request a free complete guide to selling your home or a competitive market analysis click here. If you are considering selling your home or looking for your next, I can help!

To explore available homes in the Columbus metro, click here.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Rebecca West, interior designer and founder of Seriously Happy Homes, agrees, adding that clutter can take your space away from you.

Rebecca West, interior designer and founder of Seriously Happy Homes, agrees, adding that clutter can take your space away from you. “I certainly think that people will be looking beyond the footprint of their home. Walkable neighborhoods and outdoor spaces are more important than they were pre-pandemic. It’s about the home, but it’s also about what’s outside your home. Do you have an outside gazebo or some outdoor space where you could have friends over if you’re worried about social distancing?”

“I certainly think that people will be looking beyond the footprint of their home. Walkable neighborhoods and outdoor spaces are more important than they were pre-pandemic. It’s about the home, but it’s also about what’s outside your home. Do you have an outside gazebo or some outdoor space where you could have friends over if you’re worried about social distancing?”

Augustin recommends giving thought to what makes your house really feel like home to you. “If you can continue to use the same furniture, or look at the same art, that increases feelings of familiarity and safety,” she says. “Is your furniture or your art going to fit in the new home? If you’re coming from an apartment with lots of solid, interior walls, and you go to a home that’s open plan, with very few interior walls and lots of windows, you’re not going to be able to hang as many paintings. If that art is meaningful to you, a new home where you can’t put it up and see it is not going to be the best place for you to be.

Augustin recommends giving thought to what makes your house really feel like home to you. “If you can continue to use the same furniture, or look at the same art, that increases feelings of familiarity and safety,” she says. “Is your furniture or your art going to fit in the new home? If you’re coming from an apartment with lots of solid, interior walls, and you go to a home that’s open plan, with very few interior walls and lots of windows, you’re not going to be able to hang as many paintings. If that art is meaningful to you, a new home where you can’t put it up and see it is not going to be the best place for you to be.

There were 2,875 new listings added to the Columbus and Central Ohio Regional MLS in September, and the total inventory of homes for sale in the MLS sits at 3,624, slightly lower than the 3,806 homes available one year ago.

There were 2,875 new listings added to the Columbus and Central Ohio Regional MLS in September, and the total inventory of homes for sale in the MLS sits at 3,624, slightly lower than the 3,806 homes available one year ago.

Homes in the Hilliard CSD School District (CSD) covering Hilliard and parts of Prairie Township saw just 97 closings in April versus 109 in 2022, an 11% drop year-over-year. For the year, the market area is down 10.8% with just 298 homes sold versus 334 in 2022. Predictably, the average price, $378,706, and median , $385,000, prices were both up in April compared to last year. Along with the price and interest increases, days on market expanded from 5 days to 13 days.

Homes in the Hilliard CSD School District (CSD) covering Hilliard and parts of Prairie Township saw just 97 closings in April versus 109 in 2022, an 11% drop year-over-year. For the year, the market area is down 10.8% with just 298 homes sold versus 334 in 2022. Predictably, the average price, $378,706, and median , $385,000, prices were both up in April compared to last year. Along with the price and interest increases, days on market expanded from 5 days to 13 days.